How we helped a fintech platform go decentralized and launch in five countries at once

Table of Contents

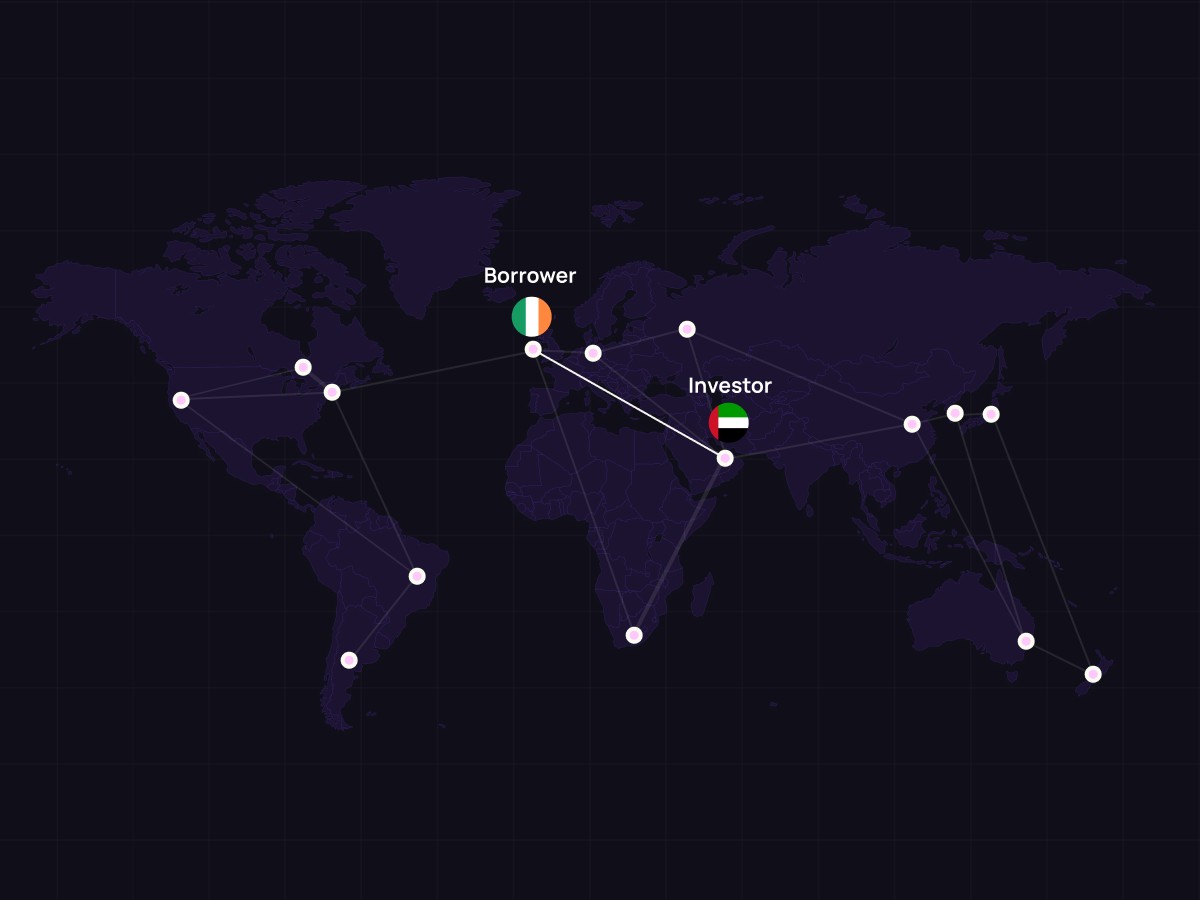

Expanding a crowdlending platform internationally usually takes years. Endless approvals, mountains of paperwork, and a new license for every country. We took a different path. Together with a Swiss fintech team, we built a decentralized platform where investors and businesses meet directly from anywhere in the world, with no banks in the middle and without the bureaucracy that slows everything down.

Moving from a local platform to a global ecosystem

Hi, I’m Anton Efimenko, a managing partner at 8Blocks. Our work helps companies earn with blockchain. We create tokenomics, design product mechanics, and turn tokens, NFTs, and game economies into profit.

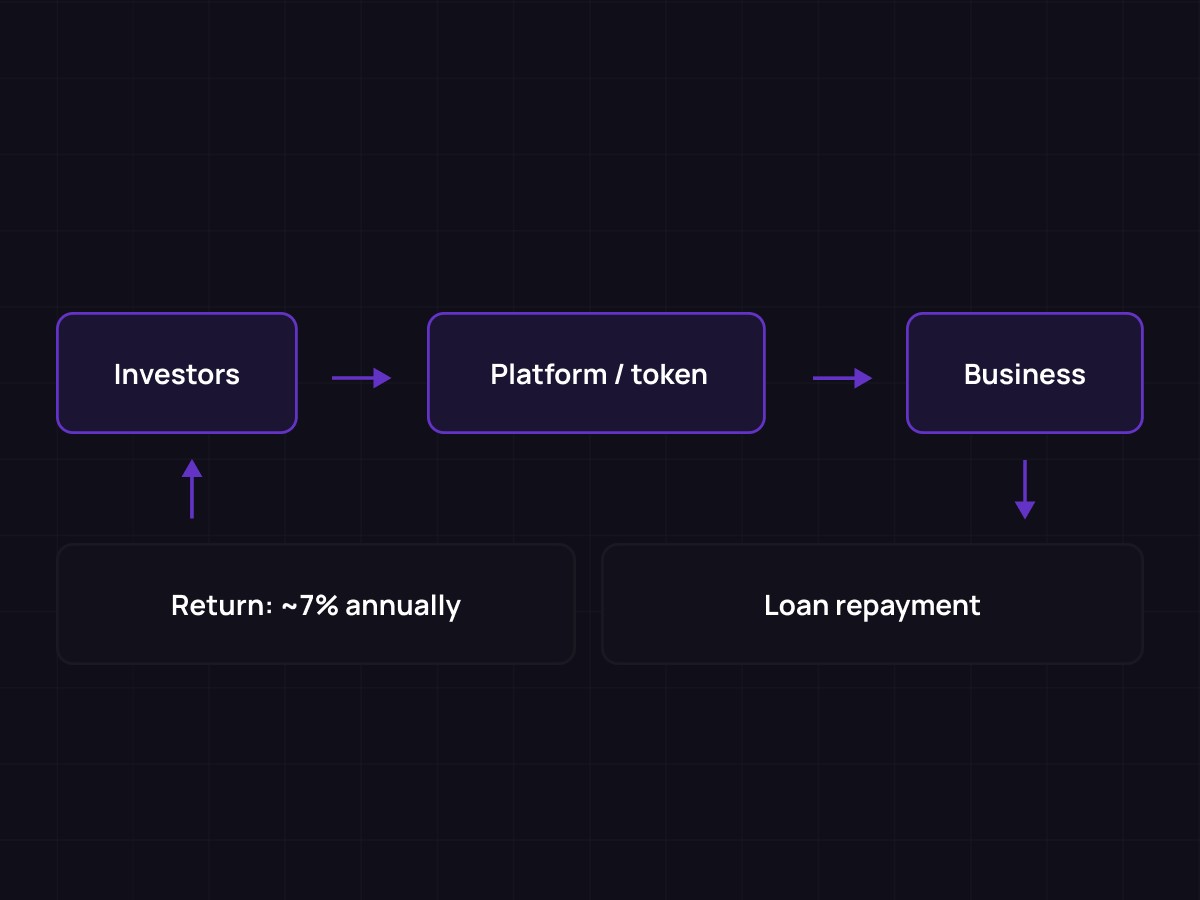

Their service allows private and institutional investors to finance companies directly without going through banks.

Here is how it works: a company submits a loan request, for example, to upgrade equipment or expand production. Investors contribute amounts starting from a few thousand francs, and the business receives the funding it needs at a fixed interest rate that averages around 7% per year.

The model worked well and stayed transparent, but within Switzerland it ran into a clear limitation. Returns were low and the regulation was tight. Investors wanted more flexibility, and companies needed wider access to capital.

Why the traditional path doesn’t scale

In the traditional model, a crowdlending platform has to go through a long and expensive process to enter a new country. Every jurisdiction has its own rules, licenses, and requirements for companies that work with investments and loans.

For a company entering the Russian market, where returns can reach 33% a year and draw strong investor interest, the process is far from simple. It starts with registering a local entity, appointing a director, and building a local team.

After that, the company must place at least 5 million rubles on deposit with the Central Bank to demonstrate financial stability.

In Russia, crowdlending platforms must also hold a nominee account. It is a dedicated banking setup that moves all funds between investors and borrowers and keeps every transaction in one controlled flow.

Only a few banks in the country provide these accounts, and getting connected to one is far from simple. The platform has to be integrated with the bank’s system, tested for full synchronization, and then cleared by the Central Bank.

The reality is that operating in even three countries requires three regulatory cycles, full reporting setup, local bank accounts, new teams, and months of approvals.

How we designed the tokenomics and avoided the pitfalls other platforms faced

Before we launched the decentralized platform, we took a close look at the market. A few teams had already tried to bring Web3 crowdlending to life, but almost none of them gained real traction.

Two issues kept blocking their progress:

Weak tokenomics. Their tokens had no clear value logic and no reliable way for investors to earn.

No investor protection. Borrowers could walk away with the funds, and the platforms had no mechanism to recover money across borders.

To keep the launch structured, the first step was to build the tokenomics from scratch. That meant defining the token’s role, shaping the logic of investor returns, and setting up how investors and borrowers interact inside the model.

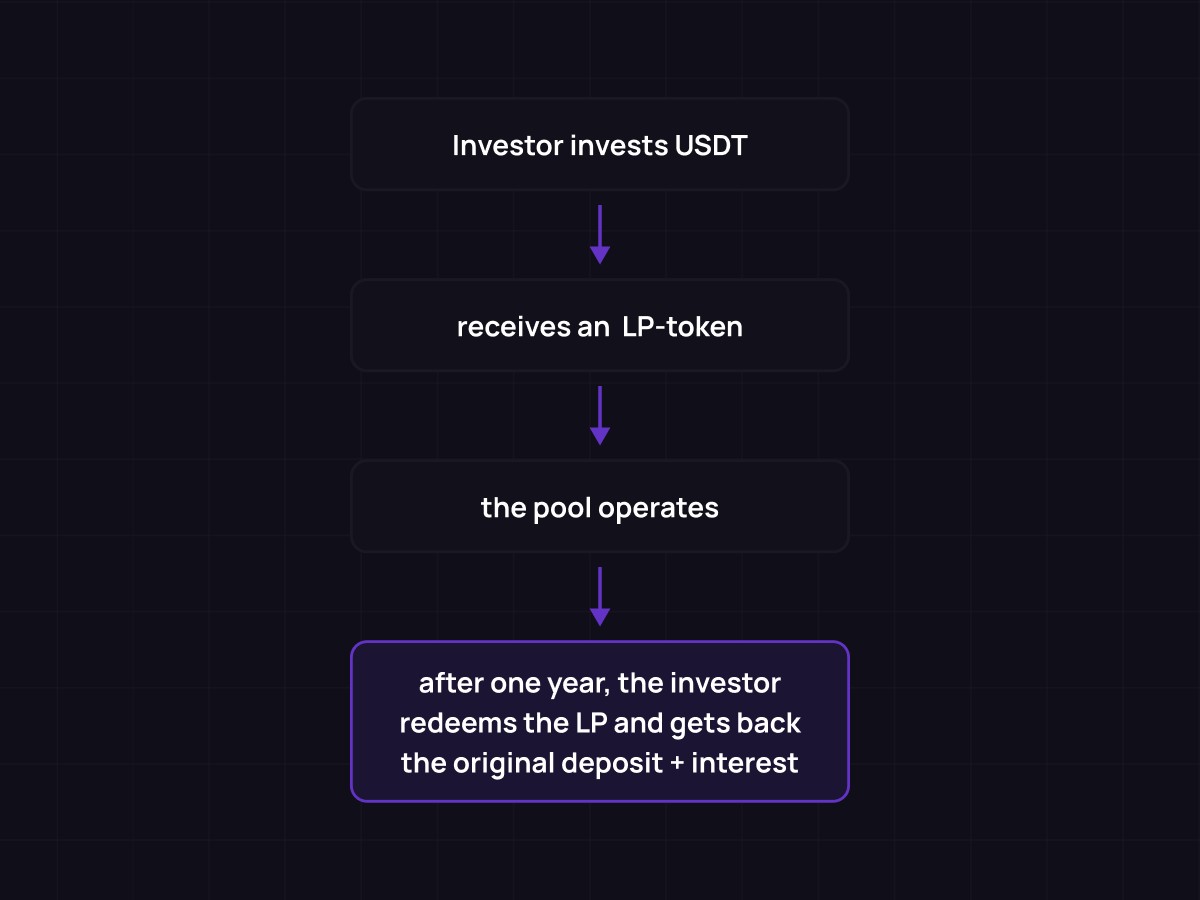

The first version of the tokenomics used a familiar DeFi setup. Investors put in USDT and received an LP token that showed their funds were in the pool. After a year, they could redeem that LP token and take back their deposit plus interest.

We needed to avoid that regulatory classification and build a model that stayed legal and scalable, which meant reworking the token architecture entirely. This redesign eventually led to a new model that we explain in the next section.

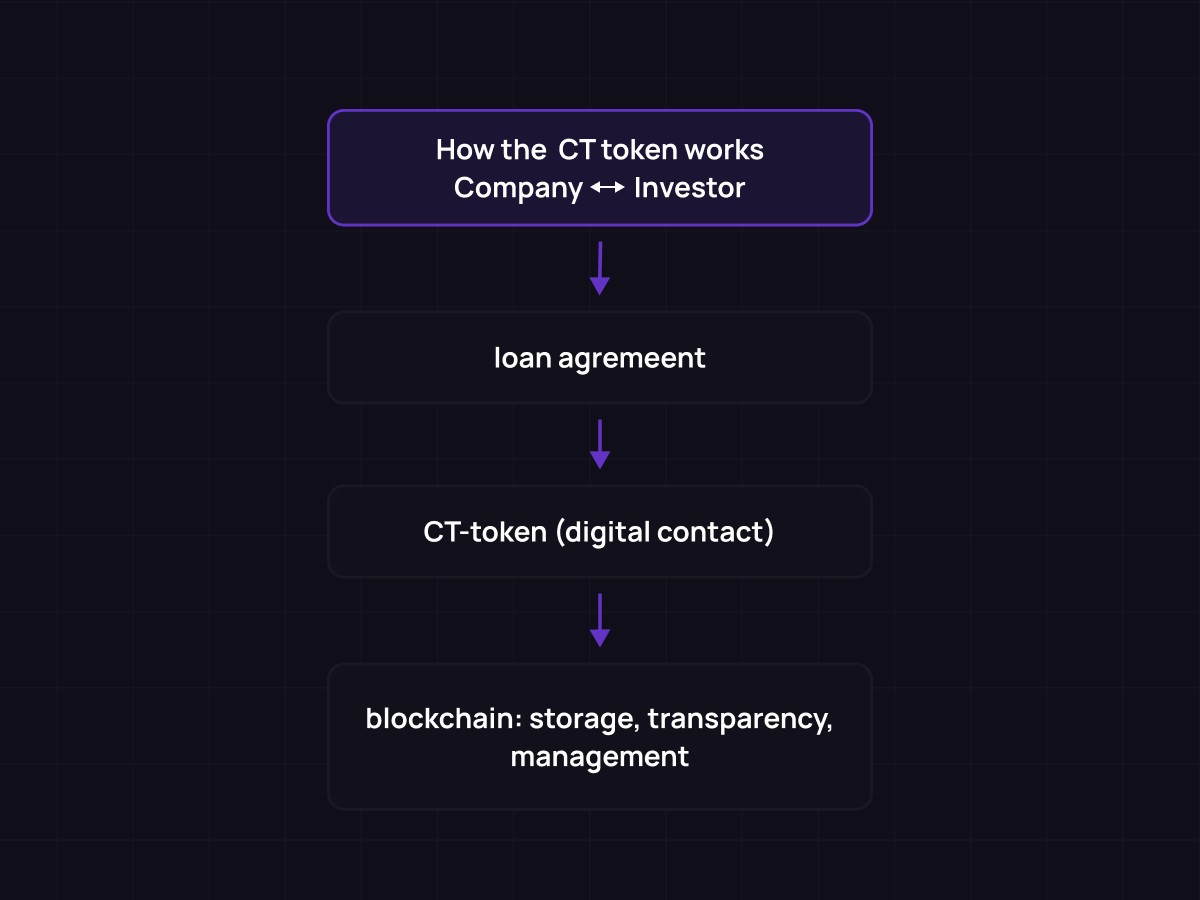

The CT token that bridged blockchain with the real economy

Unlike typical cryptocurrencies, it isn't traded on exchanges and has no market price. Its role isn't to generate profit but to simply record the investment itself: the amount contributed, the duration, and the project it was allocated to.

In simple terms, the CT token works as a digital record of a loan. It is the element that brings real transactions between companies and investors onto the blockchain and makes them fully trackable.

The project’s main token stayed purely functional. It works inside the platform to handle transactions, pay for due-diligence checks, give access to the secondary market, and support smart-contract operations. In practice, it serves as a utility token, not an investment asset.

Solving the repayment challenge

With the new tokenomics in place, the next task was to make sure investments could actually be repaid. That is where Web3 crowdlending runs into its biggest issue. A borrower can be anywhere in the world, and if a company takes the money and fails to return it, recovering the debt across borders is almost impossible.

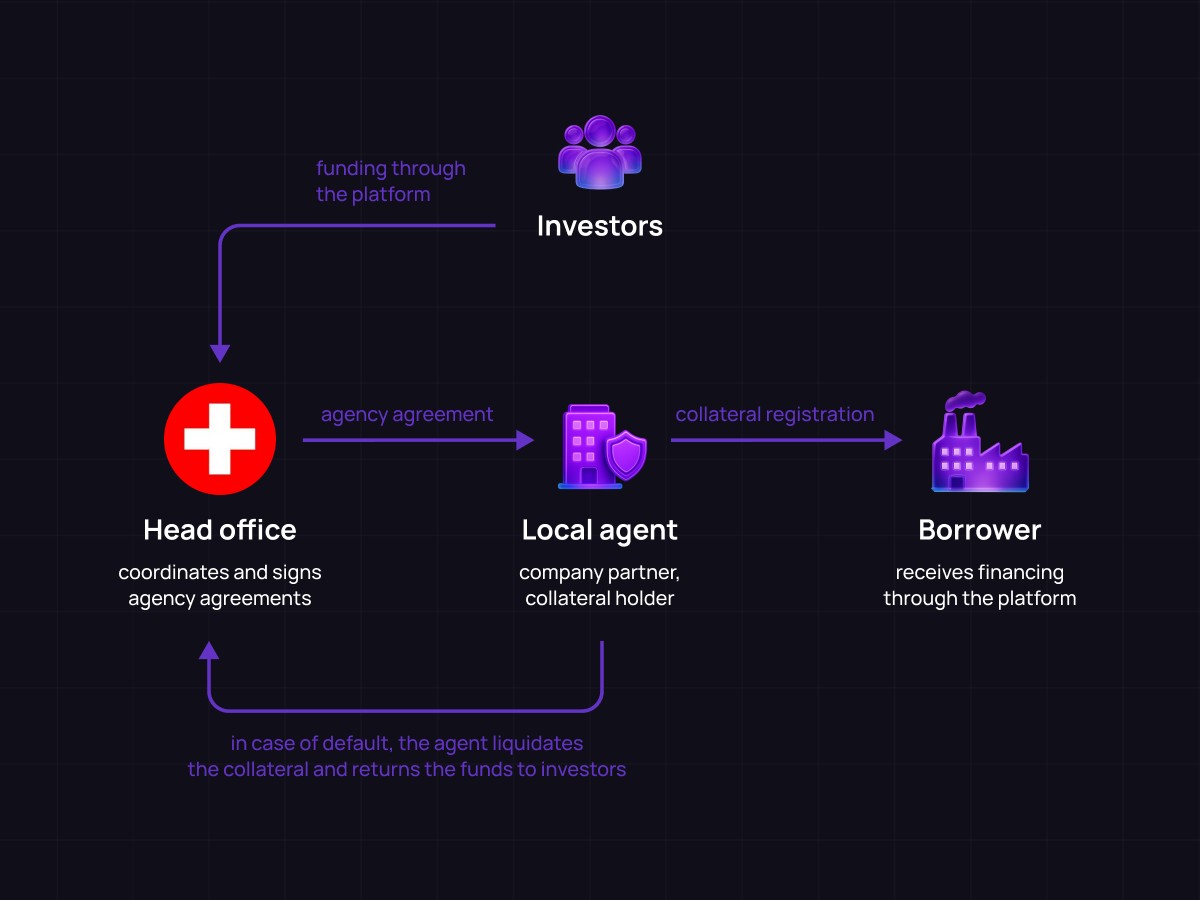

This is how the system operates:

In every country where the platform operates, a local agent joins the system. This is a partner company that represents the platform on the ground.

The agent works directly with our client’s Swiss entity under an agency agreement.

When a local business takes a loan on the platform, the collateral is registered in the name of that agent.

If a borrower fails to repay the loan, the agent can take the collateral, sell it, for example, at an auction, and use the proceeds to cover the outstanding amount. This means the agent acts as both the guarantor and the party responsible for making sure investors get their money back.

How the platform protects investor funds

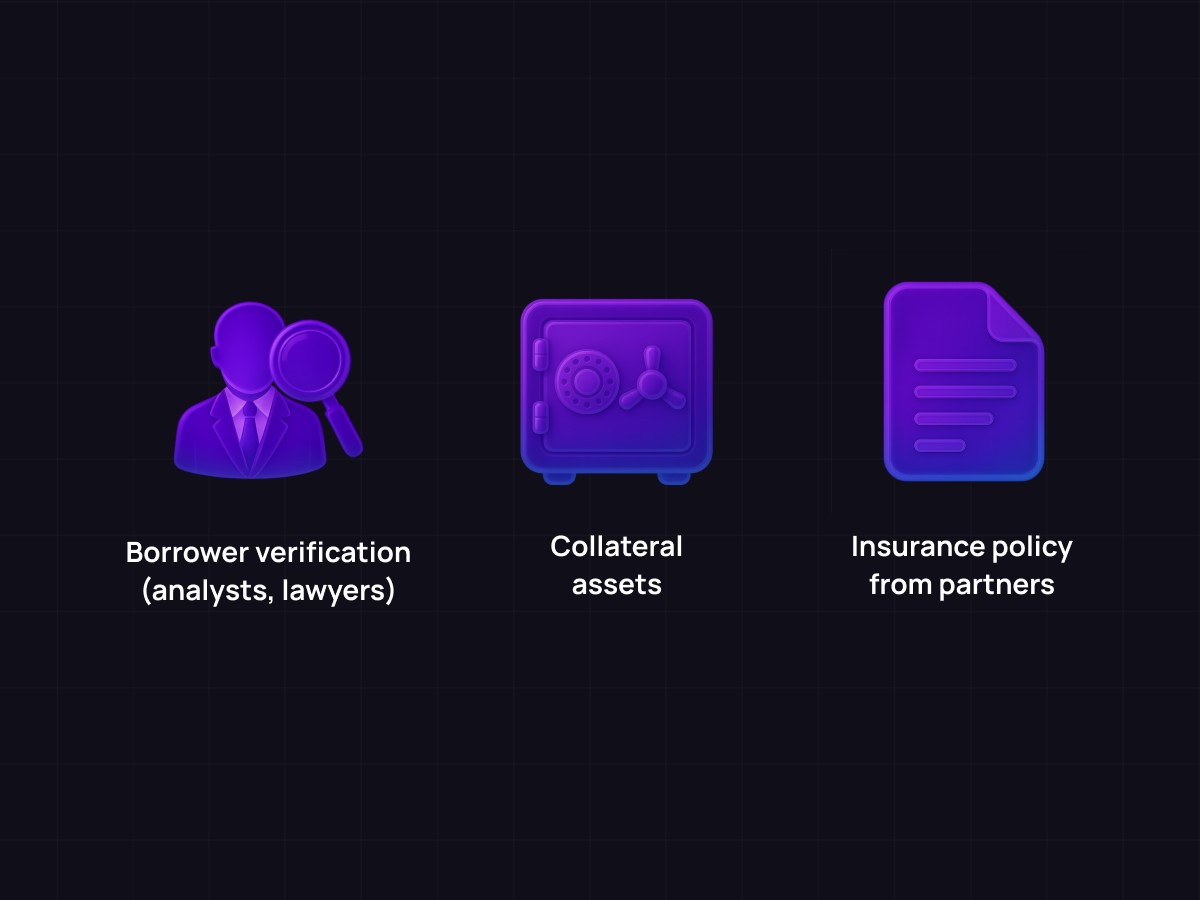

Once the collateral mechanism was in place, we strengthened investor protection by adding an insurance layer. The platform brought in insurance partners so that every investor can secure coverage in case a borrower defaults.

This is how a full insurance layer took shape inside the platform, giving every deal an additional level of protection.

Our client also relies on their own expertise. A team of analysts and lawyers carefully reviews each borrower before approval. As a result, the Swiss platform has recorded zero defaults, and even the Web3 version, which has been live for less than a year, hasn’t had a single missed repayment.

Early results: real projects and active investment

The decentralized version of the platform launched only 5 months ago, yet it already hosts real companies from Bulgaria, Georgia, Kenya, Saudi Arabia, and the UAE.

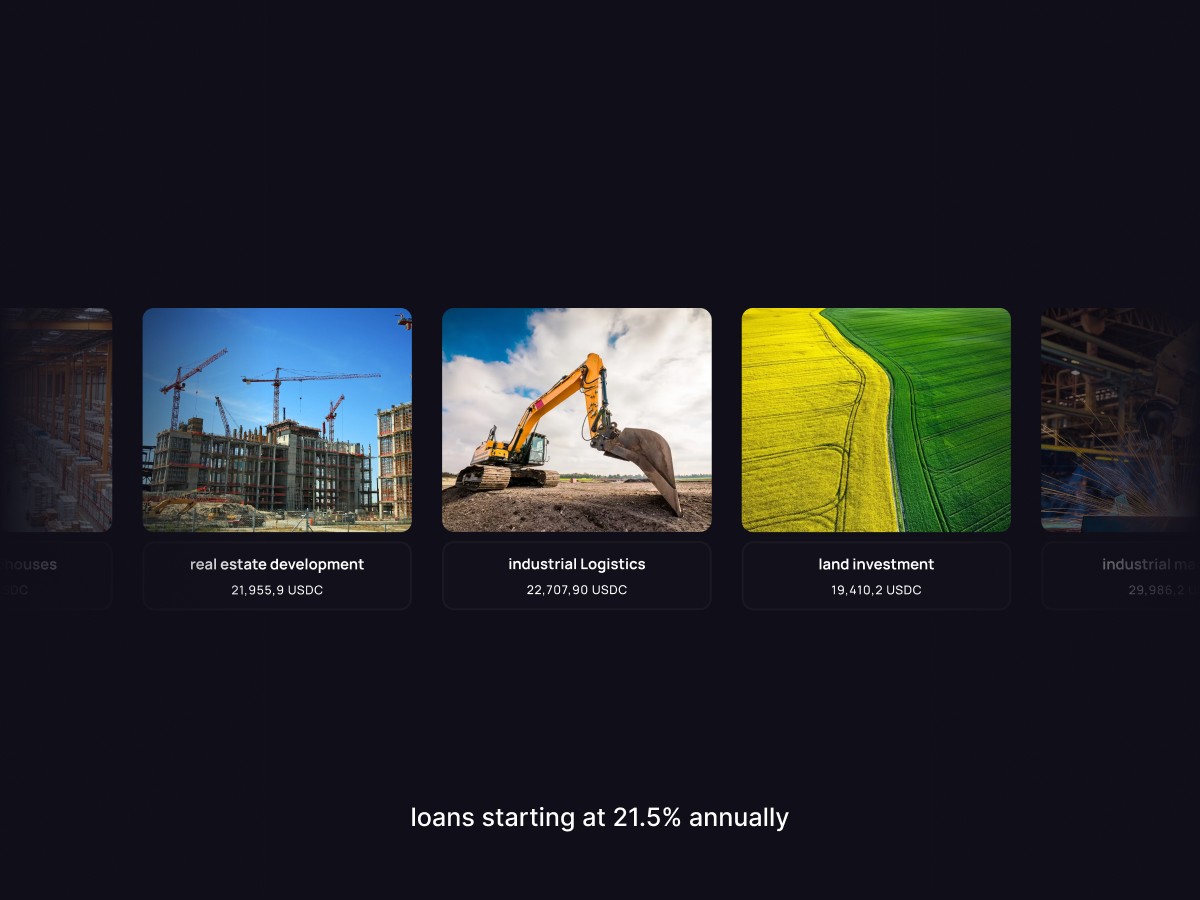

Investors can directly invest in the following projects:

Consumer Loans (Bulgaria)

Loans at 21.5% annually for a 4-month term.Strawberry Cultivation (Georgia)

Strawberry farming with a 21.9% annual return over 12 months.Mango Wholesale (Kenya)

Wholesale fruit trading with a 23.3% annual return over 8 months.Gold Car Rent (UAE)

Car rentals in Dubai with a 23.1% annual return over 9 months.Coffee Equipment (Kenya)

Coffee equipment financing with a 23.5% annual return over 8 months.

All investments on the platform are made in USDC, a stablecoin tied to the US dollar. Once a project reaches its full funding amount, the money is sent to the borrower automatically.

Why businesses borrow through the platform

At first glance, it may seem unusual: why would a company take money at around 20% per year when bank loans are cheaper? The answer depends on the type of business. The companies that come to our client’s platform aren’t startups. They are small and medium-sized businesses that are already operating and growing faster than banks can approve new credit.

Imagine a company that gets a 10 million-ruble loan from a bank, completes the project, and sees that it could easily take on another 50 to 100 million. The bank won’t extend more credit because the limit is already reached and, on paper, the company looks over-borrowed. At that point, the business starts looking elsewhere – private investors, partners, or a crowdlending platform.

A high rate isn’t a sign of risk. It simply shows that the business is active, profitable, and growing faster than banks are willing to finance.

And this is only the beginning. Our project shows that Web3 doesn’t have to be about speculation. It can operate as real infrastructure for the global economy.

Share